Cartoon workingman reluctantly paying taxes. (Photo: AdobeStock/PPD/Adiano)

The best budget rule in the United States is Colorado’s Taxpayer Bill of Rights. Known as TABOR, this provision in the state’s constitution says revenues can’t grow faster than population plus inflation. Any revenue greater than that amount must be returned to taxpayers.

Combined with the state’s requirement for a balanced budget, this means Colorado has a de facto spending cap  (similar to what exists in Switzerland and Hong Kong).

(similar to what exists in Switzerland and Hong Kong).

The second-best budget rule is probably a requirement that tax increases can’t be imposed without a supermajority vote by the legislature.

The underlying theory is very simple. It won’t be easy for politicians to increase the burden of government spending if they can’t also raise taxes. Particularly since states generally have some form of rule requiring a balanced budget.

Basically a version of “Starve the Beast.”

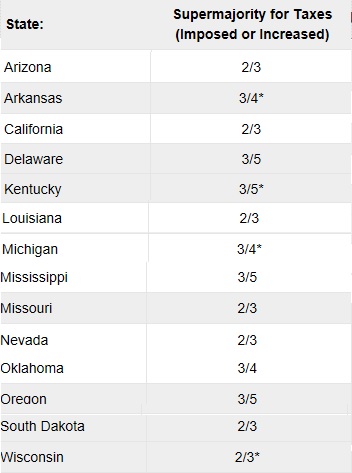

Anyhow, according to the National Council of State Legislatures, 14 states have some type of supermajority requirements.

And more states are considering this reform.

Here are some excerpts from a column in the Washington Post.

Florida Republicans are pursuing a plan to make it harder for lawmakers to raise taxes in the state, adding new hurdles for Democrats hoping to enact bold social programs such as “Medicare for all” and more robust education spending. …Florida’s Republican lawmakers have approved a ballot measure that,

if approved by the voters, would require a two-thirds “supermajority” of the legislature to enact any new taxes. …In…additional states — …Oregon and North Carolina — conservative lawmakers and business groups are currently advancing similar measures… The supermajority requirements have proved effective at keeping taxes low in the states where they have been implemented, said Joel Griffith of the American Legislative Exchange Council… “These supermajority rules make policymaking incredibly difficult,” said Elaine Maag, senior research associate at the Tax Policy Center, a nonpartisan think tank. “If a state can’t increase spending because of these very high bars for raising taxes, they can’t expand programs.”

Dean Stansel crunched the numbers in 1998 and got some encouraging data.

There is some evidence that supermajority requirements have at least helped to restrain the growth of taxes. From 1980 to 1996, state tax burdens as a share of personal income

increased by 1.1 percent in states with supermajority requirements. Taxes rose five times faster in states without such requirements. In 10 states, residents face higher top personal income tax rates today than they did in 1990. None of those states require supermajority approval for tax hikes. None of the 13 supermajority states have higher top rates today than they did in 1990, and three of them have lowered their top rate in the 1990s.

Academic experts also have found positive effects.

In a 1990 study published in the William and Mary Law Review, Jim Miller and Mark Crain found some evidence of modest spending restraint.

Seven states require approval of tax proposals by a super-majority vote in the legislature. …According to this hypothesis, the amount of revenue available to politicians resembles a budget constraint,

and when this constraint shifts, government spending consequently changes. …the tax-and-spend literature suggests a causal connection that should be controlled. This variable is expected to produce a negative coefficient because in making an increase in revenues more difficult, the requirement tightens the total constraint on spending options. …The super-majority required to increase taxes variable is negative, as expected, although it is significant at only the 10% level in the three models.

In a 2000 study published in the Journal of Public Economics, Brian Knight also determined that supermajority provisions limited taxation.

This paper measures the effect of state-level supermajority requirements for tax increases on tax rates. …A model is presented in which legislatures controlled by a pro-tax party adopt a supermajority requirement

to reduce the majority party agenda control. The propensity of pro-tax states to adopt supermajority requirements results in an underestimate of the true effect of these requirements on taxes. To correct this identification problem, the paper first uses fixed effects to control for unobserved attitudes and then employs instruments that measure the difficulty of amending state constitutions. The paper concludes that supermajority requirements have significantly reduced taxes.

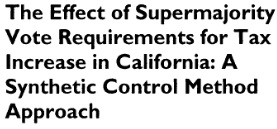

In a 2014 study published in State Politics & Policy Quarterly, Soomi Lee concluded that a supermajority has restrained the fiscal burden in California.

My article examines whether supermajority vote requirements (SMVR) to raise taxes in California’s constitution suppresses state tax burdens. The rationale behind the rule

is to contain the growth of government by making it costly to form a winning coalition to raise taxes. …I take a different approach from extant literature and estimate the causal effect of SMVR by using synthetic control methods. The results show that, from 1979 to 2008, SMVR reduced the state nonproperty tax burden by an average of $1.44 per $100 of personal income, which is equivalent to 21% of the total tax burden for each year. The effect…has abated over time.

This last study is remarkable. The long-run fiscal outlook is quite grim in California, so just imagine how much worse it would be if the supermajority requirement didn’t exist.

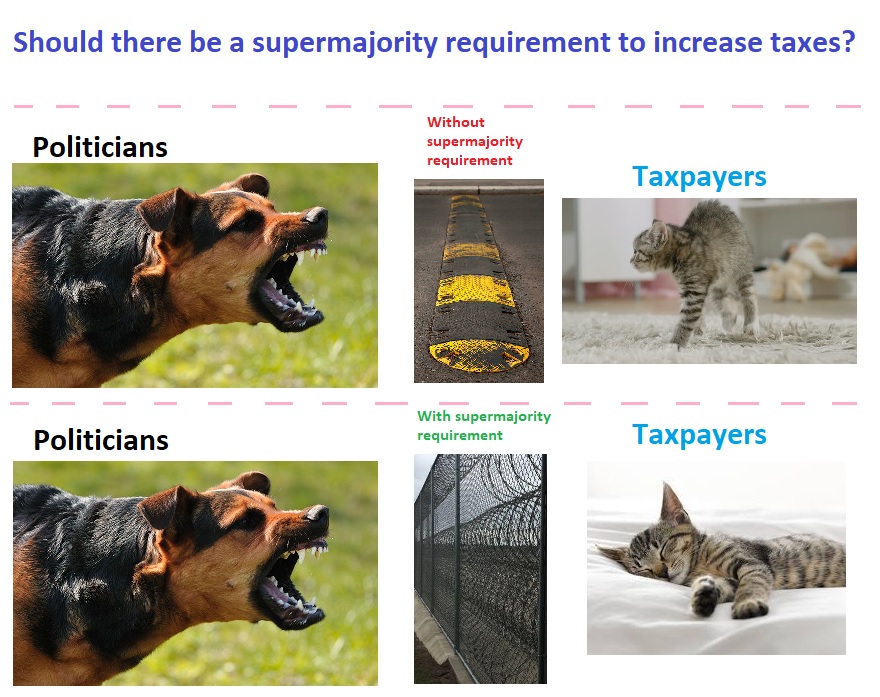

I’ll close with this amateurish visual that I created.

Though the evidence from California shows the kitten shouldn’t be peacefully sleeping if there is a supermajority requirement.

The best way to think of such a provision is that it is akin to putting locks on your doors in a crime-ridden neighborhood. The crooks may figure out how to mug you on the street or break through your windows, so you’re still in danger.

But having locks on your doors is definitely better than not having them.