Statue of Liberty in front of the New York City skyline.

I wrote yesterday about the most recent OECD numbers on “Average Individual Consumption” in member nations.

There was a very clear lesson in that data about the dangers of excessive government. The United States was at the top in this measure of household living standards,  not because American policies are great, but rather because huge welfare states in Europe have undermined economic vitality on the other side of the Atlantic.

not because American policies are great, but rather because huge welfare states in Europe have undermined economic vitality on the other side of the Atlantic.

Indeed, the only countries even remotely close to the United States were oil-rich Norway and the two tax havens of Switzerland and Luxembourg.

Those AIC numbers gave us an interesting snapshot of relative living standards in 2014.

But what would we discover if we looked at how that data has changed over time?

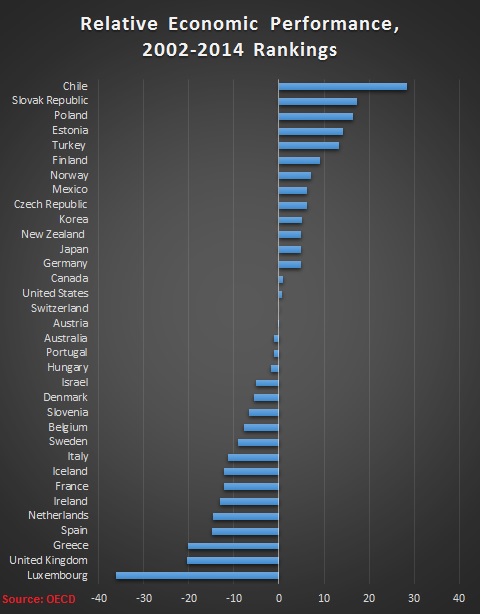

It appears that the OECD began assembling that data back in 2002. Here’s a table showing how nations rose or fell, relative to other OECD nations, since then. Based on convergence theory, one would expect to see that poorer nations enjoyed the biggest relative gains, while richer nations fell in the rankings. And that is what generally happened, but with some notable exceptions.

Here are the countries that did not conform, for either good reasons or bad reasons, to convergence theory.

We’ll start with the nations that have bragging rights.

- Chile started at the very bottom compared to the rich nations of the western world, so anything other than a large increase would have been a disappointment. But the magnitude of Chile’s increase is nonetheless quite impressive and presumably a testament to pro-market reforms.

- Finland was almost 7 points below the OECD average in 2002 and now is more than 2 points above the average, which is a significant jump for a nation near the middle of the pack. Maybe having sensible leaders is a good idea.

- Oil-rich Norway was above average at the start of the period and even farther above average at the end of the period.

- The United States was very high in 2002 and remained very high in 2014. Since that outcome violates convergence theory, that’s a non-trivial accomplishment and another piece of evidence that big governments in Europe are imposing a harsh economic cost.

- Switzerland also started high and remained high. That’s presumably a reflection of good policies such as federalism and spending restraint.

Now for the nations that did not fare well.

- Luxembourg suffered a large drop, some of which is understandable since the tiny tax haven was in first place back in 2002. But the magnitude of the decline – particularly compared to the United States and Switzerland – is not an encouraging sign. This may be a sign that anti-tax competition efforts by the OECD have hit the nation hard.

- Greece, Spain, Ireland, and Italy all tumbled in the rankings even though – at best – they started in the middle of the pack. It will be interesting to see how these nations perform as they recover (or don’t recover, as I expect in the cases of Italy and Greece) from the European fiscal crisis.

- Slovenia also went from bad to worse, which perhaps is not a big surprise since it is one of the least reform-oriented countries to emerge from the Soviet Bloc.

- The United Kingdom suffered a rather large decline, almost all of which happened under the profligate Blair and Brown Labour governments. This will be another nation that will be interesting to watch in coming years, particularly because of Brexit.

- France and the Netherlands also suffered, starting well above average in 2002 but falling to the mean in 2014.

If you like this kind of data on whether nations are trending in the right direction or wrong direction, I’ve also tinkered with the data from Economic Freedom of the World.

Last year, I highlighted countries that have made significant moves in the EFW rankings, including oft-overlooked success stories such as Israel and New Zealand.

Last year, I highlighted countries that have made significant moves in the EFW rankings, including oft-overlooked success stories such as Israel and New Zealand.

I also looked specifically at changes in Europe this century and did not find any reason for optimism.

The bottom line is that there’s no substitute for free markets and limited government. If nations want faster growth and more prosperity, they need to mimic jurisdictions such as Hong Kong and Singapore.

Unfortunately, there’s very little reason to be optimistic about that happening in Europe.