International Monetary Fund (IMF) headquarters. (Photo: Reuters)

Since I’ve written that the International Monetary Fund (IMF) is “the Dumpster Fire of the Global Economy” and “the Dr. Kevorkian of Global Economic Policy,” I don’t think anyone could call me a fan of that international bureaucracy.

But I’ve also noted that the real problem with organizations like the IMF is that they have bad leadership. The professional economists at international bureaucracies often produce good theoretical and empirical work. That sensible research doesn’t make much difference, though, since the actual real-world policy decisions are made by political hacks with a statist orientation.

For instance, the economists at the IMF have produced research on the benefits of smaller government and spending caps. But the political leadership at the IMF routinely ignores that sensible research and instead has a dismal track record of pushing for tax increases.

Hope springs eternal, though, so I’m going to share some new IMF research on tax policy that is very sound. It’s from the second chapter of the bureaucracy’s newest Fiscal Monitor. Here are some excerpts, starting with an explanation of why the efficient allocation of resources is so important for prosperity.

A top challenge facing policymakers today is how to raise productivity, the key driver of living standards over the long term. …The IMF’s policy agenda has therefore emphasized the need to employ all policy levers, and in particular to promote growth-friendly fiscal policies that will boost productivity and potential output. Total factor productivity (TFP) at the country level reflects the productivity of individual firms…aggregate TFP depends on firms’ individual TFP and also on how available resources (labor and capital) are allocated across firms. Indeed, the poor use of existing resources within countries—referred to here as resource misallocation—has been found to be an important source of differences in TFP levels across countries and over time. …What is resource misallocation? Simply put, it is the poor distribution of resources across firms, reducing the total output that can be obtained from existing capital and labor.

The chapter notes that creative destruction plays a vital role in growth.

Baily, Hulten, and Campbell (1992) find that 50 percent of manufacturing productivity growth in the United States during the 1980s can be attributed to the reallocation of factors across plants and to firm entry and exit. Similarly, Barnett and others (2014) find that labor reallocation across firms explained 48 percent of labor productivity growth for most sectors in the U.K. economy in the five years prior to 2007.

And a better tax system would enable some of that growth by creating a level playing field.

Simply stated, you want people in the private sector to make decisions based on what makes economic sense rather than because they’re taking advantage of some bizarre quirk in the tax code.

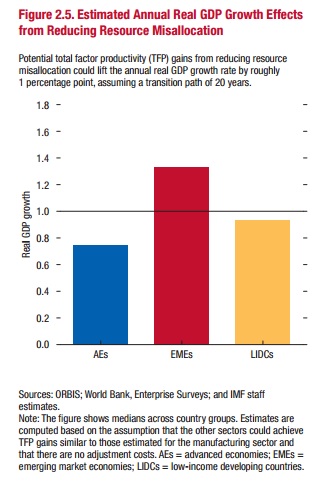

Potential TFP gains from reducing resource misallocation are substantial and could lift the annual real GDP growth rate by roughly 1 percentage point. …Upgrading the design of their tax systems can help countries chip away at resource misallocation by ensuring that firms’ decisions are made for business and not tax reasons. Governments can eliminate distortions that they themselves have created. …For instance, the current debt bias feature of some tax systems not only distorts financing decisions but hampers productivity as well, especially in the case of advanced economies. …Empirical evidence shows that greater tax disparity across capital asset types is associated with higher misallocation.

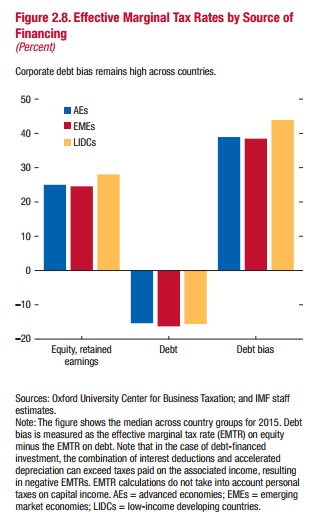

One of the main problems identified by the IMF experts is the tax bias for debt.

And since I wrote about this problem recently, I’m glad to see that there is widespread agreement on the economic harm that is created.

Corporate debt bias occurs when firms are allowed to deduct interest expenses, but not returns to equity, in calculating corporate tax liability.

…Several options are available to eliminate the distortions arising from corporate debt bias and from tax disparities across capital asset types, including the allowance for corporate equity system and a cash flow tax. …In the simplest sense, a CFT is a tax levied on the money entering the business less the money leaving the business. A CFT entails immediate expensing of all investment expenditures (that is, 100 percent first-year depreciation allowances) and no deductibility of either interest payments or dividends. Therefore, if it is well designed and implemented, a CFT does not affect the decision to invest or the scale of investment, and it does not discriminate across sources of financing.

By the way, regular readers may notice that the IMF economists favor a cash-flow tax, which is basically how the business side of the flat tax operates. There is full expensing in that kind of system, and interest and dividends are treated equally.

This is also the approach in the House Better Way tax plan, so the consensus for cash-flow taxation is very broad (though the House wants a destination-based approach, which is misguided for several reasons).

But let’s not digress. There’s one other aspect of the IMF chapter that is worthy of attention. There’s explicit discussion of how high tax rates undermine tax compliance, which is music to my ears.

Several studies have shown that tax policy and tax administration affect the prevalence of informality and thus productivity. Colombia provides an interesting case study on the effect of taxation on informality. A 2012 tax reform that reduced payroll taxes was found to incentivize a shift of Colombian workers out of informal into formal employment. Leal Ordóñez (2014) finds that taxes and regulations play an important role in explaining informality in Mexico. For Brazil, Fajnzylber, Maloney, and Montes-Rojas (2011) show that tax reductions and simplification led to a significant increase in formal firms with higher levels of revenue and profits. While a higher tax burden contributes to the prevalence of informality… For 130 developing countries, a higher corporate tax rate is found to increase the prevalence of cheats among small manufacturing firms, lowering the share of sales reported for tax purposes.

In closing, I should point out that the IMF chapter is not perfect.

For instance, even though it cites research about how high tax rates reduce compliance, the chapter doesn’t push for lower rates. Instead, it endorses more power for national tax authorities. Makes me wonder if the political folks at the IMF imposed that recommendation on the folks who wrote the chapter?

Regardless, the overall analysis of the chapter is quite sound. It’s based on a proper understanding that growth is generated by the efficient allocation of labor and capital, and it recognizes that bad tax policy undermines that process by distorting incentives for productive behavior.

The next step is convince Ms. Lagarde and the rest of the IMF’s leadership to read the chapter. They get tax-free salaries, so is it too much to ask that they stop pushing for higher taxes on the rest of us?