From left to right: Senate Majority Leader Mitch McConnell, R-Kty., Sen. Orrin Hatch, R-Utah, Treasury Secretary Steve Mnuchin and Director of the National Economic Council Gary Cohn introduce the Republican tax reform plan at the U.S. Capitol in Washington, U.S., November 9, 2017. (Photo: Reuters)

Back on November 2, I summarized the good and not-so-good features of the tax plan put forth by House Republicans. Here are the parts that made me happy.

- Lower corporate tax rate.

- Ending the deduction for state and local income taxes.

- Death tax repeal.

And what was the most disappointing part of the plan?

- Absence of spending restraint.

Regarding my disappointment, I’m not just being a curmudgeonly libertarian. The bill is filled with timid and convoluted provisions, as well as some undesirable revenue-raising provisions, precisely because of congressional rules on long-run deficit neutrality. As I’ve noted in some of my TV interviews, Republicans are pushing sub-par policy because you can’t fit a football player’s body into Pee Wee Herman’s clothes.

If Republicans were willing to impose some modest spending restraint — by contrast — that would have given them enormous flexibility for large tax cuts, while also balancing the budget.

But I’m a semi-realist about Washington. I’m not going to make the perfect the enemy of the good (or, in this case, the sort-of-decent the enemy of the I-guess-this-is-acceptable).

Now let’s look at what Senate Republicans have unveiled. In some cases, my grades are identical to the House bill because many of the major provisions are quite similar. But there are some noteworthy differences.

Lower corporate rate: A-

America’s high corporate tax rate is probably the most self-destructive feature of the current system. If the rate is permanently reduced from 35 percent to 20 percent, that will be a huge boost to competitiveness. The only downside is that the lower rate is deferred until 2019.

Lower individual rates: C+

The proposal is relatively timid on rate reductions for households. This is disappointing, but not unexpected since lower individual tax rates mean considerable revenue loss.

Ending deduction for state and local taxes: A+

Next to the lower corporate tax rate, this is the best part of the proposal. It generates revenue to use for pro-growth provisions while also eliminating a subsidy for bad policy on the part of state and local governments. Indeed, the Senate bill goes farther than the House bill since it includes property taxes. So I’ve retroactively changed my grade for the House bill from A+ to A- so I can give the Senate bill an A+.

Curtailing mortgage interest deduction: C

The deduction remains for home mortgages, but is curtailed for home equity loans. A timed improvement that will only slightly reduce the distortion that creates a bias for residential real estate compared to business investment.

Death tax repeal: C+

There’s no repeal. Just an increase in the amount of family savings that can be protected from the tax. Better than nothing, to be sure, but disappointing.

Change to consumer price index: C

It is quite likely that the consumer price index overstates inflation because it doesn’t properly capture increases in the quality of goods and service. Shifting to a different price index will lead to higher revenues because tax brackets and other provisions of the tax code won’t adjust at the same rate. That’s fine, but I’m dissatisfied with this provision since it should apply to spending programs as well as the tax code.

Reduced business interest deduction: C+

The business interest deduction is partially undone, which is a step toward equal treatment of debt and equity. It’s not the right way of achieving that goal, but it does generate revenue to finance other pro-growth changes in the legislation.

Now let’s zoom out and grade the overall plan in terms of major fiscal and economic goals.

And you’ll see that all I’ve done is repeat exactly what I wrote about the House bill.

Restraining the growth of government: F

In my fantasy world, I want a return to the very small federal government created and envisioned by the Founding Fathers. In the real world, I simply hope for a modest bit of spending restraint. This legislation doesn’t even pretend to curtail the growth of government, which is unfortunate since some fiscal prudence (federal budget growing about 2 percent per year) would have allowed a very large tax cut while also balancing the budget within 10 years.

Collecting revenue in a less-destructive manner: B

This is a positive proposal. It will mean more jobs, increased competitiveness, and higher incomes. The wonks in Washington doubtlessly will debate whether these positive effects are small or large, but I’m not overly fixated on that issue. Yes, I think the growth effects will be significant, but I also realize that many other policies also determine economic performance. The most important thing to understand, thought is that even small increases in growth make a big difference over time.

Now let’s take a closer look at how the House and Senate plans differ.

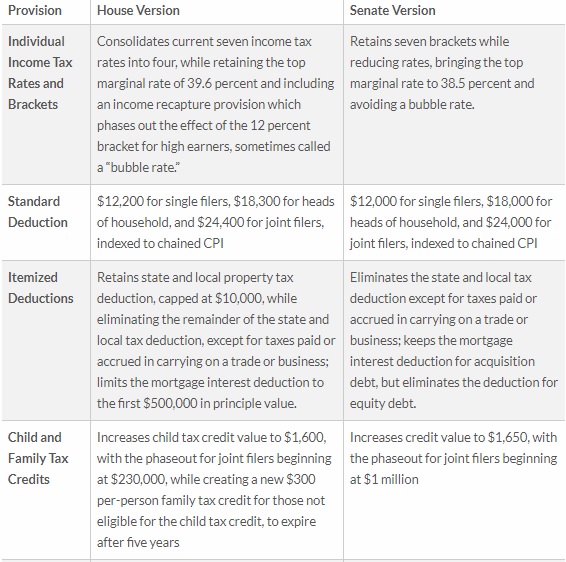

The Tax Foundation put together a very helpful comparison. I’ve broken it into three parts so I can interject some final commentary.

For this first section, since I already gave my two cents about itemized deductions, I’ll simply observe that the Senate plan is slightly better on individual income tax rates.

For this second section, I’ll merely note that the first provision is basically an attempt to give relief to small businesses that are subject to the individual income tax.

The provisions are complicated because it’s not easy to lower tax rates for “Schedule C” income in a way that doesn’t benefit taxpayers who aren’t perceived as being conventional small businesses.

For this final section, the part that’s disappointing to me is “international income.” Both the House and Senate adopt territorial taxation for businesses, which is very good.

But the congressional plans then claw back a bunch of money with OECD-style “base-erosion” policies and Obama-style global minimum taxes. It’s unclear if the net effect is modestly positive or modestly negative, but it’s not what many of us wanted when we pushed for territoriality.

I’ll close by noting that I’m actually pleasantly surprised by the two plans. Yes, I’m grading on a curve, but I had very low expectations this year. I basically hoped to get a lower corporate rate with a bit of window dressing.

And at one point we were actually forced to play defense because Republicans were looking at a very troubling proposal for a “border-adjusted tax.”

So even though I fantasize about a flat tax, I’m reasonably happy about where we are now.

The bottom line is that there’s now a good chance of getting legislation that drops the corporate rate to 20 percent while also eliminating the deduction for state and local income taxes. Those are two very good policies. And if we somehow get death tax repeal, that means three substantive, pro-growth reforms. Fingers crossed.